This luggage leader is staging a turnaround. But can it overcome its baggage?

VIP’s market share dropped, inventory piled up, and debt increased, weighing on the stock’s performance.

The company’s share price hit a 52-week low of ₹248 on 7 April—a level last seen during the pandemic—down from the stock’s all-time high of ₹775 that it reached on 1 April 2022.

To arrest the slide, VIP initiated a restructuring that included an inventory liquidation and a balance sheet repair. These efforts are now showing early signs of revival. Its share price recovered about 43% from ₹248 on 7 April to ₹355.40 at the end of trading on 27 May.

As the market leader, VIP is aiming for a turnaround in FY26. But how far has the recovery come and what lies ahead?

A hard turn

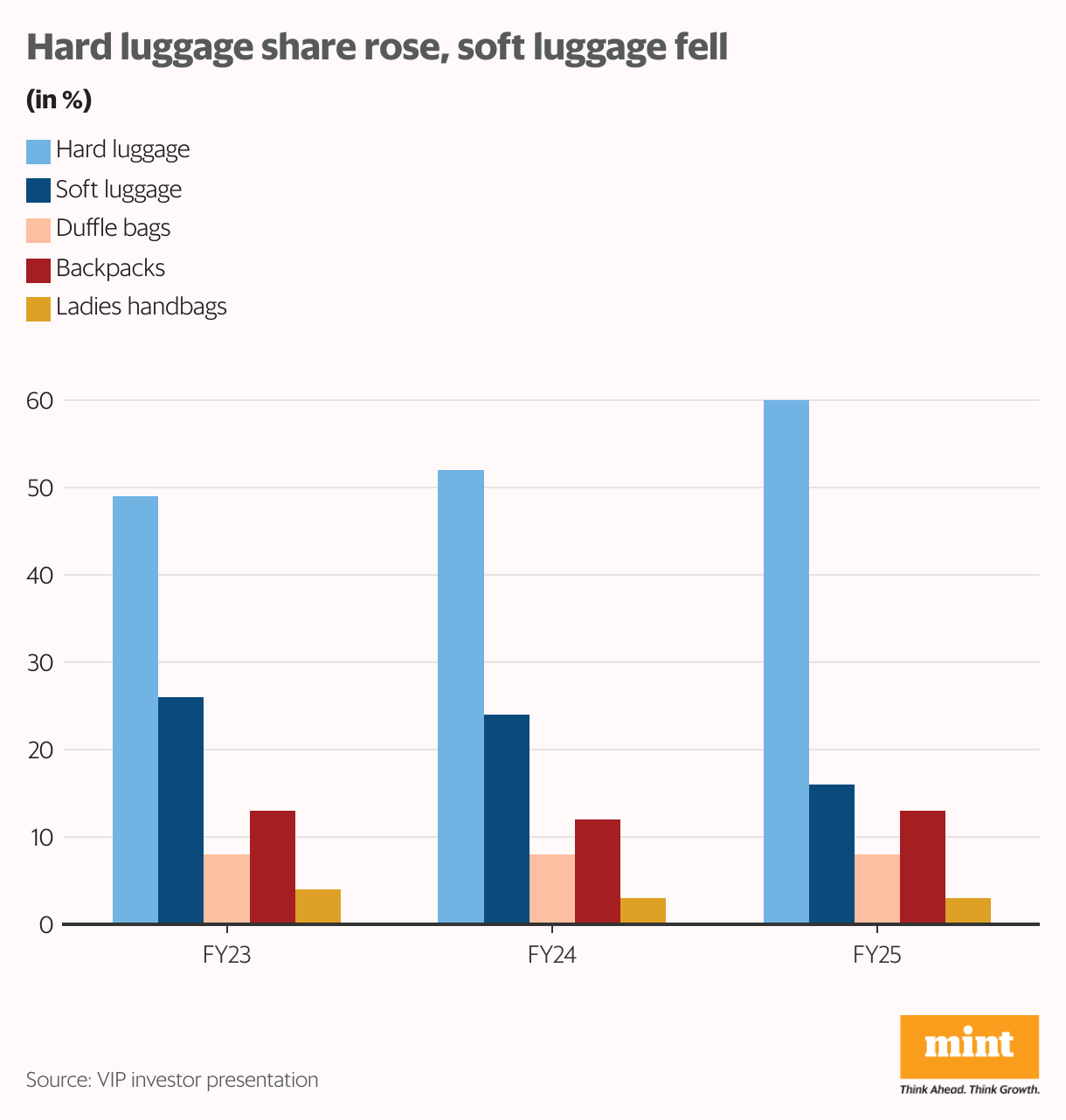

VIP’s earlier dominance came from its leadership in soft luggage, in line with customer preferences at the time. But as demand shifted towards hard luggage, this positioning turned into a headwind. Soft luggage inventory piled up due to weaker demand, while hard luggage inventory remained lean at around 15 days.

As of March 2024, VIP held inventory worth ₹916 crore. Of this, nearly ₹300 crore was soft luggage, enough to last six months given that the company was selling ₹50 crore worth of luggage each month.

Yet, VIP chose not to aggressively discount the stock on its inventory as most of it was relatively new. Demand didn’t pick up meaningfully, hurting performance.

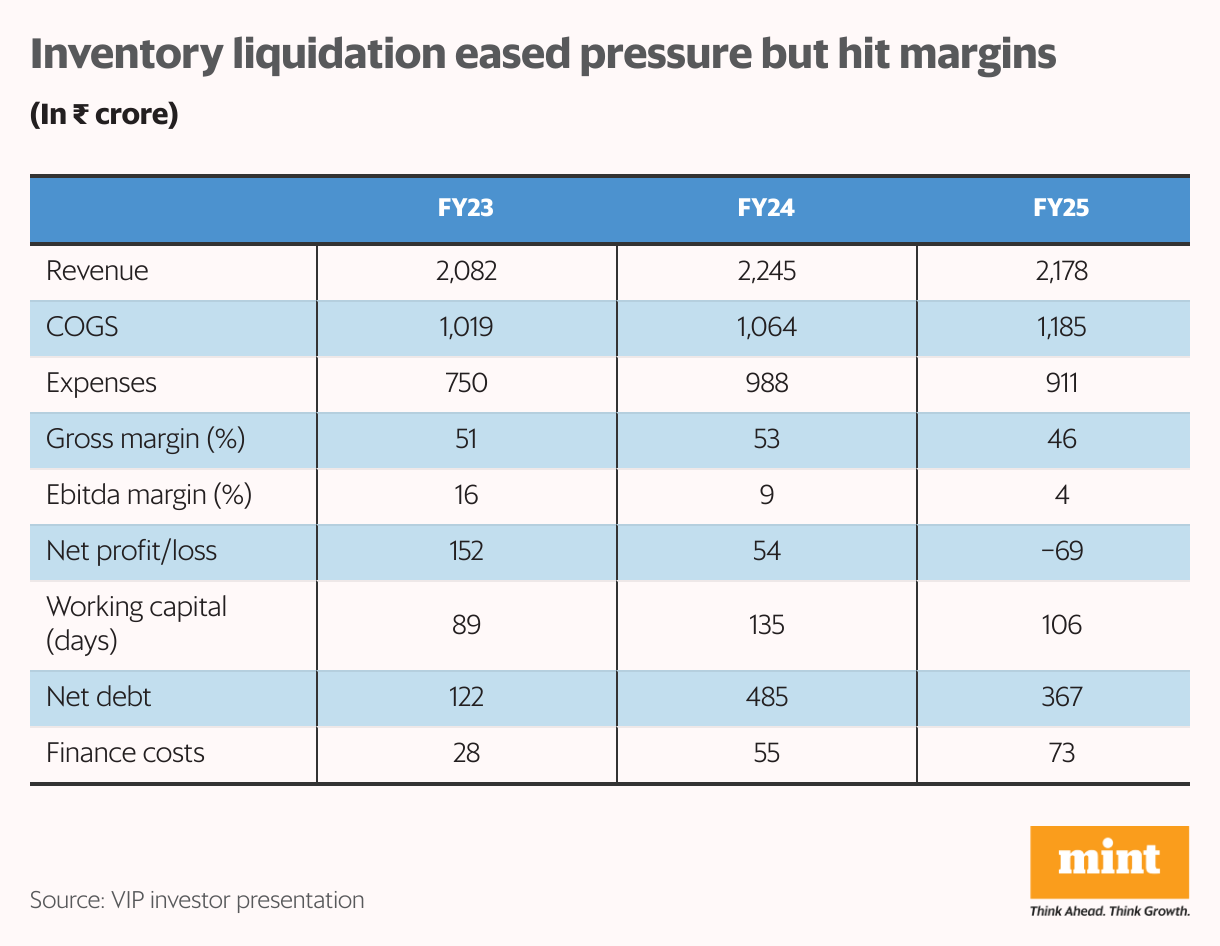

This was reflected in the numbers. VIP’s Ebitda margin dropped 670 basis points to 9.1% in FY24 as sales growth lagged and fixed costs surged. Net profit fell 65%. Working capital days rose from 89 in March 2023 to 135 in March 2024.

To fund operations, borrowings increased sharply. Net debt surged nearly 4x to ₹485 crore in March 2024, up from ₹122 crore a year earlier. Finance costs doubled from ₹28 crore to ₹55 crore.

Meanwhile, competitors adapted faster. Safari had already pivoted to hard luggage, giving it an edge. Both Safari and Samsonite gradually gained market share at VIP’s expense. VIP’s market share declined from 47% in 2020 to 38% in 2024, while Safari’s market share increased from 25% to 32% in this period.

At the same time, VIP was slower in scaling e-commerce, which made it harder to move inventory. The build-up in inventory and working capital needs, coupled with aggressive discounting by new-age brands, added further pressure to recovery efforts.

An operational reset

These challenges prompted business restructuring. VIP brought in the Boston Consulting Group to lead the restructuring, which was aimed at market share growth, margin recovery, revenue growth, cost optimization, and debt reduction.

Consequently, VIP discontinued production of upright soft luggage and started liquidating soft luggage stock at discounted prices. At the same time, VIP shifted its focus to premiumization, e-commerce growth, and hard luggage.

In FY25, VIP reduced its inventory by ₹218 crore, mainly from the ₹300 crore soft luggage pile. Inventory volumes declined from 6.3 million pieces in FY24 to 3.8 million by the end of FY25.

With leaner inventory, VIP’s sales volume increased 11% in FY25. However, price growth lagged behind volume growth due to lower realization from inventory liquidation at discounted prices. Revenue grew only 3% to ₹2,178 crore in FY25.

But with the liquidation phase nearing its end, revenue is likely to improve as sales begin to normalize at better realizations. Additionally, growth will benefit from a low base in FY25.

Also read | Trent’s 1,000% rally takes a breather. Can a Sensex rejig revive its fortunes?

Margin erosion followed inventory liquidation

The impact of liquidation was more profound on VIP’s margins. Gross margin fell 660 basis points to 46% in FY25, weighed by lower realization. Ebitda margin declined to 4% from 19% as the cost of goods sold rose 11% to ₹1,185 crore. As margins collapsed, VIP swung to a loss of ₹69 crore in FY25 from a ₹54 crore profit in FY24.

Positive signs

VIP also focused on optimizing costs and cutting inefficiencies. It shut 133 unprofitable stores in FY25, mostly in tier 3 and 4 towns, and opened just 32 outlets in high-footfall locations. Its cost-control efforts have started to reflect in its numbers.

Total expenses dropped 8%, driven by a 20% reduction in manpower costs and a 5% decline in other expenses. Manpower now accounts for 10% of revenue, down from 12% in FY24.

The lower inventory helped reduce working capital days to 106 in March from 135 a year earlier. VIP’s cash flow from operations also increased, enabling it to repay borrowings, leading to a ₹118 crore reduction in net debt in FY25. Net debt now stands at ₹367 crore.

Category-wise salience has also improved. Soft luggage now contributes 16% of VIP’s revenue, down from 24% previously, while hard luggage accounts for 60% of its portfolio, up from 52%.

As for VIP’s distribution channels, e-commerce now accounts for 31% of the mix, registering a healthy 40% growth.

Margin recovery and premiumisation

With leaner inventory, VIP has started reducing excess warehousing. In Q4FY25, it surrendered 400,000 sq.ft. of warehouse space; another 300,000 sq.ft. is set to be released shortly. These moves are expected to support margin expansion starting this quarter (Q1FY26).

VIP aims to reduce its inventory by another ₹150 crore in FY26, alongside debt reduction. With lower debt, its financing cost should also come down, thereby increasing its profitability.

VIP now plans to hold soft-luggage inventory at natural demand levels (75,000-80,000 pieces). Management has hinted that demand for soft luggage could rebound, especially in the premium segment.

Within product categories, most product launches will continue to be in hard baggage. VIP plans to maintain its e-commerce share at 30%, meaning online and offline channels will grow equally. The company is focusing on increasing its premiumization share in e-commerce.

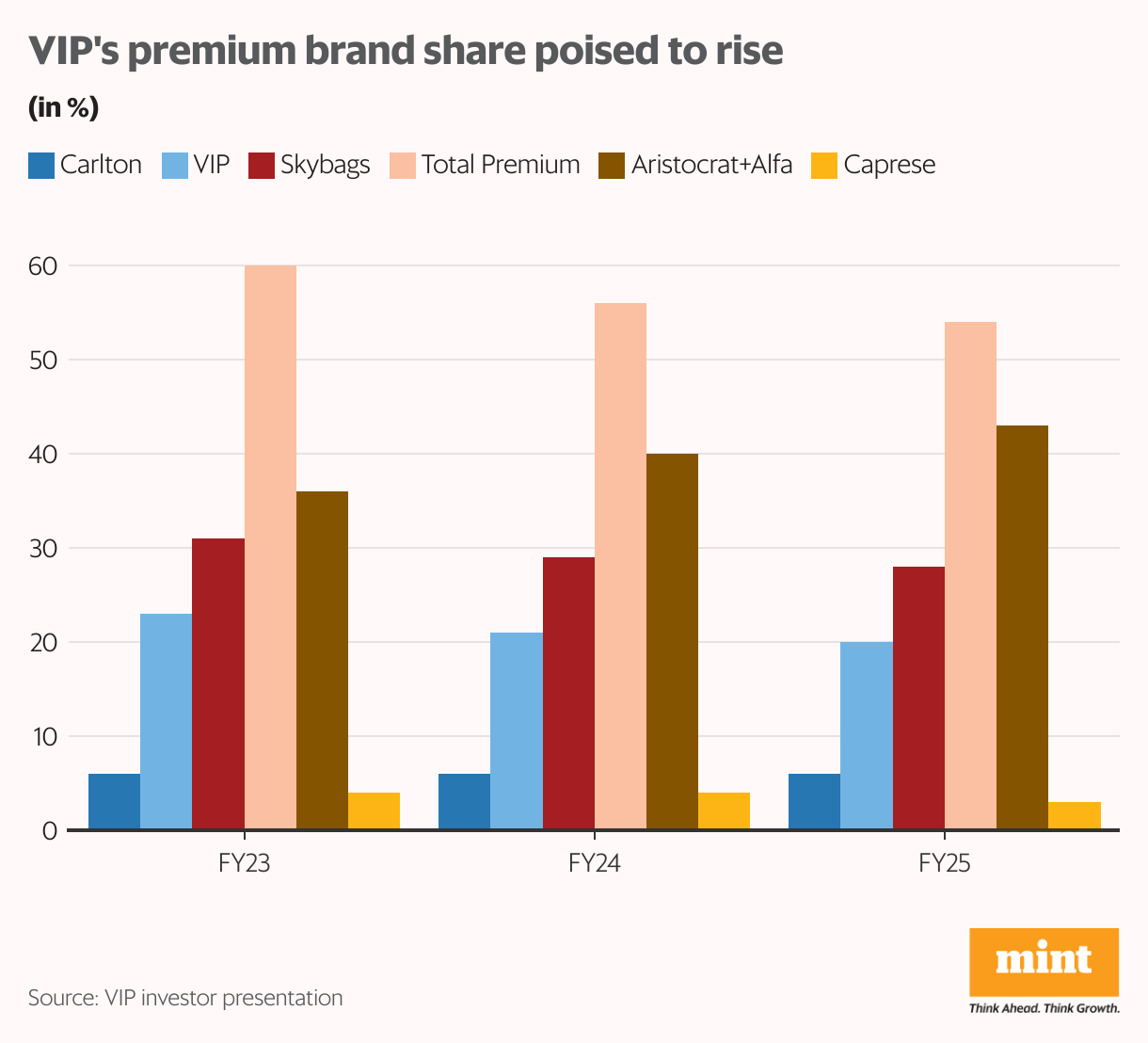

Brand-wise, the company plans to push its Carlton, VIP, and Skybags brands to grow its premium segment, which has lagged in the last 3-4 years. VIP aims to increase its share in the premium segment (excluding Aristocrat) from 54% to 60%. The company has also stepped up marketing efforts, which are yielding positive results.

VIP expects to grow faster than the industry average of 12% by 1-2 percentage points. It will focus on the top 14 cities for store expansion to ensure better store-level profitability. The company plans to open 50 stores in FY26—20 Carlton-exclusive and 30 VIP Lounge stores—targeting high-value urban markets to support premium positioning and revenues.

Valuation offers room for rerating

FY25 was a year of consolidation and operational reset for VIP Industries. While the company took a hit on margins and posted a loss, foundational fixes are in place. Management expects the benefits of restructuring to start reflecting from Q1FY26.

Meanwhile, VIP trades at a price-to-sales multiple of 2.4x, a 62% discount to Safari, which trades at 6.3x. VIP now appears better placed to ride the recovery, but a rerating will depend on sustained improvement in margins and return to profitability.

Also read | IDFC’s growth hits a speed bump. Is the stock’s bounce-back at risk?

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.