PepsiCo bottler Varun Beverages opts to expand reach as competitors in soft-drinks market engage in price war

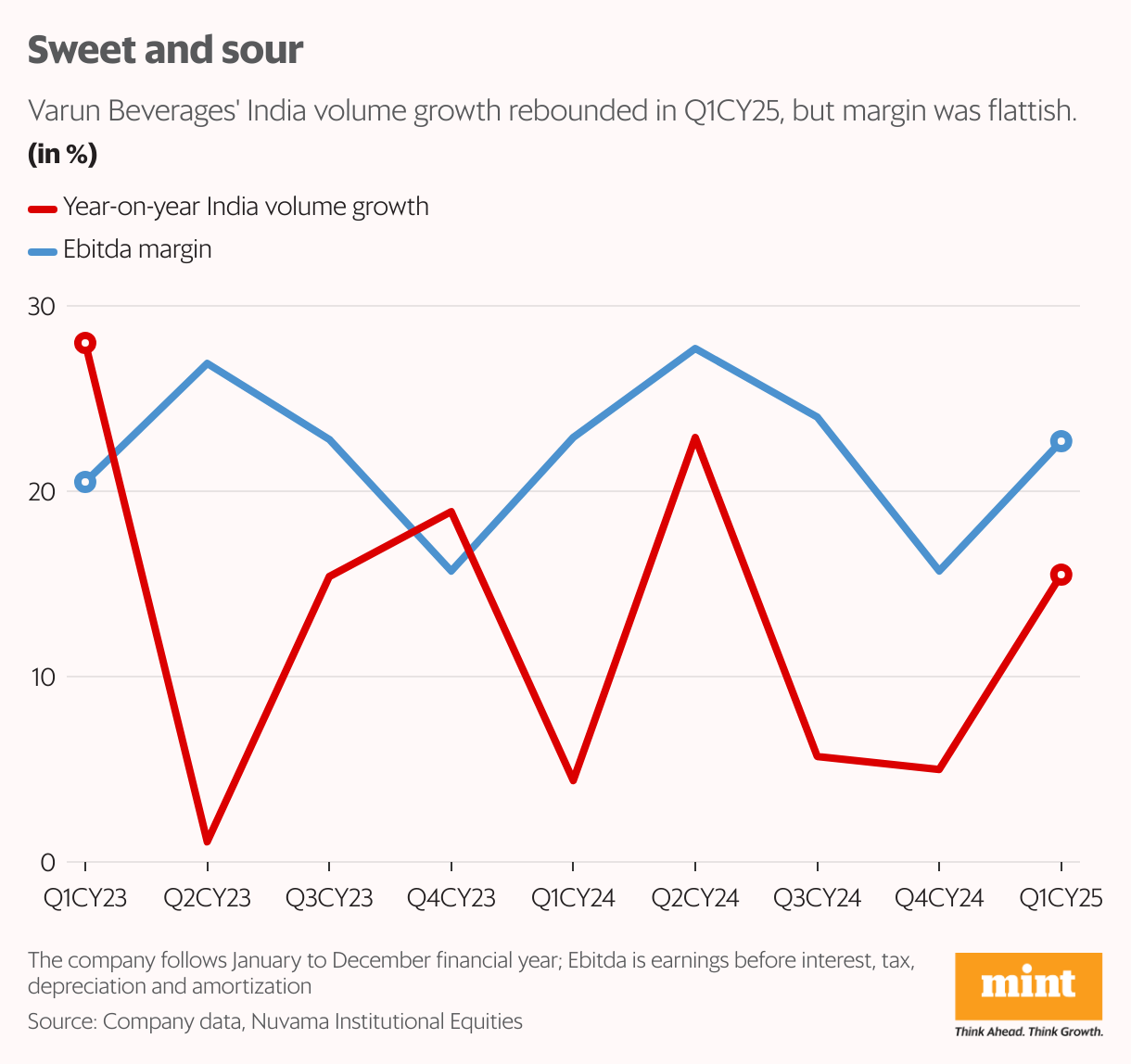

Varun Beverages Ltd (VBL) has chosen to fight the war of reach instead of pricing as competition stiffens in India’s soft drinks market. The PepsiCo bottler clocked a 30% year-on-year volume growth in the March quarter (Q1CY25), led by 15.5% organic growth in India and a deepening presence in overseas markets including South Africa and Zimbabwe. The company follows a January-to-December financial year.

“Strong double-digit volume growth in India with margin expansion should allay investor concerns around Reliance’s Campa, a key positive in Q1,” analysts at Jefferies India said in a report on 30 April, referring to the competitor’s disruptive pricing. “Although Q2CY25 is quite important from a seasonality perspective.”

India Ebitda margin rose 111 basis points (bps) due to operational efficiencies aided by volume growth. VBL’s consolidated revenue increased 29% in Q1CY25, encouraging it to guide for a double-digit growth for CY25. This despite rivals splurging on campaigns in the ongoing Indian Premier League cricket tournament and sweetening trade margins.

Nuvama Institutional Equities noted that Tata Consumer has re-indexed retailer margins in its NourishCo business to match the competition. Coca-Cola highlighted double-digit volume growth in Q1CY25, led by strong performances from Coca-Cola and Thums Up, although it reported a drop in non-alcoholic ready-to-drink beverages.

“Coca-Cola saw over 180 million servings during the Maha Kumbh Mela festival, which in our view would have helped the industry growth rate,” Nuvama’s analysts said.

Reliance Consumer has announced new plants in Bihar and Assam to ramp up its manufacturing and distribution footprint.

Distribution is key

Against this backdrop, VBL coped by doubling down on expanding its outlet coverage and cold-chain infrastructure. Its mantra: deepen market penetration and sharpen the product mix. It believes rising competition is expanding the overall category, reiterating that with only 4 million of India’s 12 million FMCG outlets covered, distribution remains a key growth lever.

VBL’s energy and hydration categories grew over 100% in Q1CY25. Value-added dairy, a new engine, also grew at 100%+, albeit on a smaller base. Smaller packs—though costlier to make—helped lift realisation per case, which rose 1.8% in India but stayed flat in the overseas markets.

On the flipside, VBL’s consolidated gross margin fell to 54.6%, down 171 basis points year-on-year. Higher volumes from South Africa hurt as a large part of sales there came from owned brands that have lower margins. Plus, overall water costs have been shifted into direct costs, while the rising share of carbonated soft drinks and smaller pack sizes pushed up the cost of goods sold.

The Ebitda margin drop of 20 bps to 22.7% was much smaller in Q1CY25. VBL continues to hold firm on its India Ebitda margin floor of 21%. The management said that while inflation and product-mix shifts could pressure the margin temporarily, its backward integration, improved scale and focus on operational efficiency give it confidence in defending profitability—even in an aggressive market.

VBL has a capex plan of ₹3,100 crore for this year. It is adding four plants, including the Bihar and Meghalaya sites set to go live in May.

Meanwhile, South Africa remains a work in progress. Volumes rose 13% year-on-year over the trailing 12 months, and Pepsi’s contribution improved from 15% to 20%. It is trimming loss-making SKUs. The South Africa business Ebitda margin improved from 10% at acquisition to 14% but is still much lower.

VBL shares fell 2% on Wednesday after the results as investors weighed the near-term pressures. Jefferies cut its earnings per share estimates by 7-9% on moderation in its assumptions on growth in the international segment and lower margin assumptions.

Even so, with the market offering enough growth potential, VBL’s bet on reach may well pay off if execution is healthy.